African Cocoa Production Market Analysis

AUTHOR BIO

Report Posted On: 2022-06-17

Prudence is our Senior Research Analyst for markets including retailing, beauty & personal care, commercial agriculture and farming across African markets. Her core expertise includes market trend analysis, brand research, competitive analysis and business planning. She has been working at Researchtec for more than 4 years, starting as Research Assistant Intern before becoming a senior analyst.

ABSTRACT

The global chocolate market is big business. It is estimated that by 2025, the market will be worth an estimated US$186billion, up from US$139billion in 2019. Thats a minute drop in the ocean when contrasted with the combined US$7billion that the two biggest cocoa producers in the world - Ivory Coast and Ghana, got in 2019/2020. These two cocoa production market giants produce more than 65% of all the global cocoa yet collected a measly 5% of the actual value of the finished chocolate product in 2019.

Despite efforts by both Ghana and Ivory Coast governments to increase farmer incomes by introducing a Living Income Differential in 2019, adding $400 to the price of a ton of cocoa so as to protect their farmers from poverty, many of the biggest chocolate producers from Big Chocolate including Mondelez, and Nestle have continued to exploit poor farmers for decades by paying very low prices for cocoa.

Furthermore, many cocoa farmers n West Africa are increasingly abandoning cocoa farming alltogether in favour of rubber, due to not just the challenge of very poor prices but also decreasing soil fertility, disease pandemics and other challenges the sector is facing.

Nevertheless, some of these challenges are clearly presenting untapped gaps in the market for companies that can offer products such as organic supplement/nutrient boosters to help boost the natural immunity and health of crops as well as increase soil productivity. Data across most African countries shows that majority of both agricultural and livestock supplements/drugs are fake. It is a major problem affecting the agricultural sector in Africa.

CITATION

Introduction

The global chocolate market is big business. It is estimated that by 2025, the market will be worth an estimated US$186billion, up from US$139billion in 2019. However, contrast that revenue with the combined US$7billion that the two biggest cocoa producers in the world - Ivory Coast and Ghana, got in 2019/2020. These two cocoa production market giants produce more than 65% of all the global cocoa in 2019 yet collected a measly 5% of the actual value of the finished chocolate product in 2019-2020.

To understand why cocoa farmers upstream earn so little, its imperative to first study the cocoa production value chain. With five levels, upstream cocoa producers are the first level and the lowest earners, followed by sourcing and marketing at the second level. This is comprised of local and global purchasing intermediaries (e.g. exporters and cocoa traders) that export both raw and semi-finished cocoa beans. Third on the value chain are the processors that process the beans (e.g. manufacturers and grinders). Fourth are the distributors including retailers. The final level downstream is occupied by the consumers.

Cocoa farmers upstream, being last on the value chain totem pole, have increasingly fetched lower prices as retailers, manufacturers and other intermediaries have taken a bigger share every subsequent year, meaning the value of cocoa beans has reduced from 50% of a chocolate bar in the 1970%, to less than 6% today.

Despite efforts by both Ghana and Ivory Coast governments to increase farmer incomes by introducing a Living Income Differential in 2019, by adding $400 to the price of a ton of cocoa so as to protect their farmers from poverty, many of the Big Chocolate producers, including Mondelez, and Nestle have continued to exploit poor farmers for decades by cleverly circumventing any such regulations to pay very low prices for raw cocoa beans.

The result is that many cocoa farmers in West Africa earn less than $1 a day. This is why many are increasingly abandoning cocoa farming alltogether in favour of rubber, due to not just the challenge of very poor prices but also decreasing soil fertility, disease pandemics and other challenges the sector is facing.

Nevertheless, for those that are staying in cocoa production, some of these challenges clearly present untapped gaps in the market even upstream. For instance, there is lot of untapped potential for companies that offer products such as organic supplement/nutrient boosters that can help boost the natural immunity and health of cocoa crops as well as those that increase soil productivity, two factors that are exacerbating an already challenging situation for cocoa farmers.

Data across most African countries shows that the majority of agricultural supplements, fertilizers as well as livestock drugs are fake. It is a major problem affecting the agricultural sector in Africa. But it also presents gaps in the market that are lucrative and commercially viable for investors.

Market Overview

Two million family farms in some of West Africa’s poorest areas produce 70 percent of the world’s cocoa. The cocoa sector is a major engine of regional economic activity, generating significant export revenue and providing livelihood for 20 million people.

According to the International Cocoa Organisation (ICCO), some three-quarters of the world’s cocoa originates from Africa, accounting for 3,556 tonnes of cocoa in the 2019/2020 season, out of a global total of 4,697 tonnes.

In Ghana, the sector employs about 800,000 farm families and generates $2 billion annually through foreign exchange earnings on the back of exports. In Côte d’Ivoire, where cocoa is the largest export crop, it accounted for 39% of exports in 2019, earning around $5 billion annually and employing about 600,000 farmers and another 6 million people across the full value chain.

Currently, Côte d’Ivoire and Ghana are the largest producers of cocoa in the world, commanding 65% of the world’s production followed by Nigeria and Cameroon. However, yields have continued to dwindle because of several factors that continue to constrain the market;

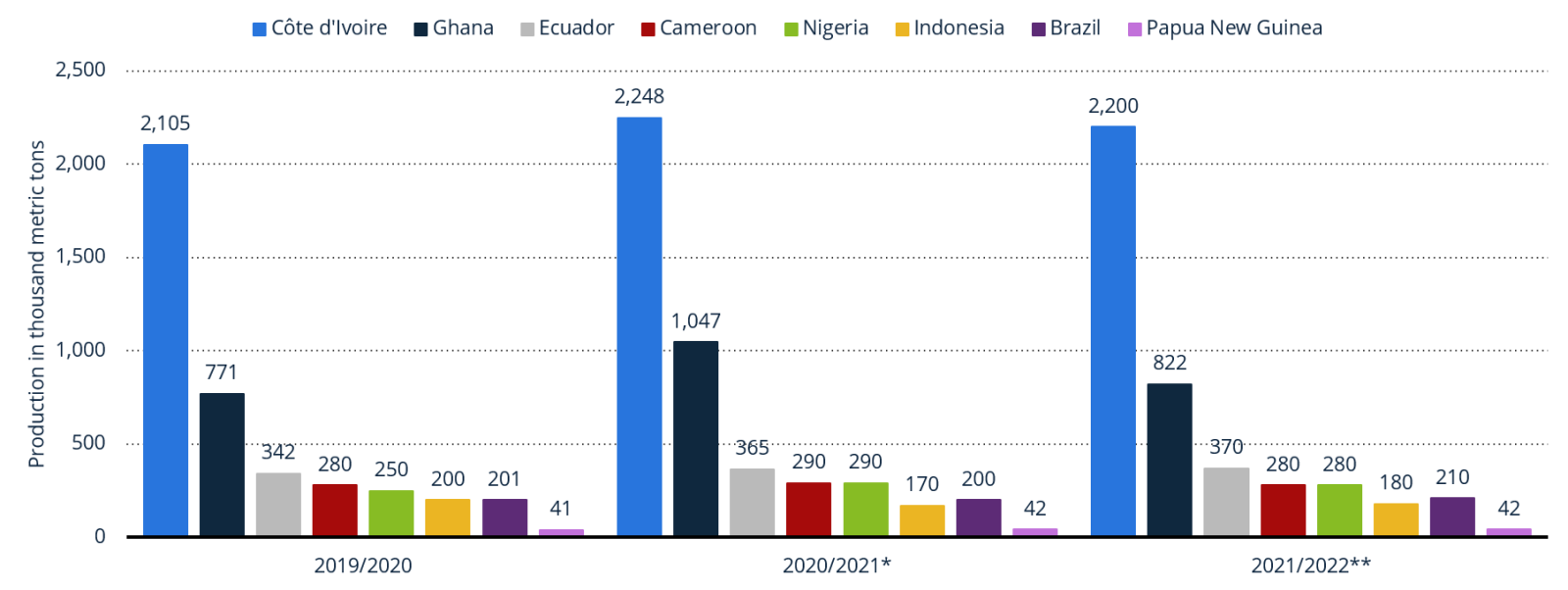

Figure 1: Annual cocoa production by country, from 2019/2020 to 2021/2022 (in 1,000 metric tons)

However, production of cocoa across the major producer countries especially in Africa has been in decline in recent times as shown by figure 1 (above).

Some of the major constraints that have faced the cocoa sector in Africa include the widespread occurrence of pests and diseases, primarily five major diseases which affect cocoa production as follows; 1) Phytophthora pod rot (black pod), 2) witches’ broom, 3) cacao swollen shoot virus, 4) vascular streak dieback, and 5) monilia pod rot.

These five diseases account for over 40% of the annual yield loss across the different production regions.

The decline in cocoa production across major producers such as Ghana can be explained by the growing diseases epidemic, which is eating up production. As earlier mentioned, at least 16% of all cocoa plants in the region are affected, yet scientists are still far from getting a permanent solution.

Furthermore, 90% of cocoa in Africa is grown on small family farms of 2 to 5 hectares, most managed by poor farmers who don’t earn enough to invest in the farms. As a result, the yield is greatly impacted by pesticides, diseases and extreme weather conditions most likely because of their poor health which can’t withstand the changing environment.

As matter of fact, most agricultural farmers in Africa are producing below their real production capacity because of pests, diseases, extreme weather environment and ofcourse poverty among farmers, which can’t allow them to afford to invest in their farms.

Recent research also shows that most pesticides used across both agricultural and even livestock farming on the African market are unregistered and fake.

These factors, combined with poor agricultural practices and poor-quality fertilizers have resulted in soil acidification, loss of organic matter, aluminium toxicity and lower soil fertility.

Nevertheless, these challenges also present an untapped gap in the market for companies that can offer natural or organic supplements/nutrients that can help boost the natural immunity and health of crops.

Cote d Ivoire’s cocoa market and value chain has massive growth potential and opportunities that can be explored further especially upstream where farmers continue to struggle with diseases, fake pesticides and poor quality soils.

Below is the research and insights into the major cocoa producers and their market opportunities, based on sound data to help you further understand the African cocoa market and its opportunities.

Ivory Coast

The West African nation of Ivory Coast accounts for around 45% of the world’s cocoa production, bringing in export revenue of $3.5 billion (CHF3.2 billion) a year.

Ivory Coast is the largest cocoa producer in both Africa and the world, supplying at least a third of the world’s total cocoa and leading the rest of the world by more than half a million tonnes.

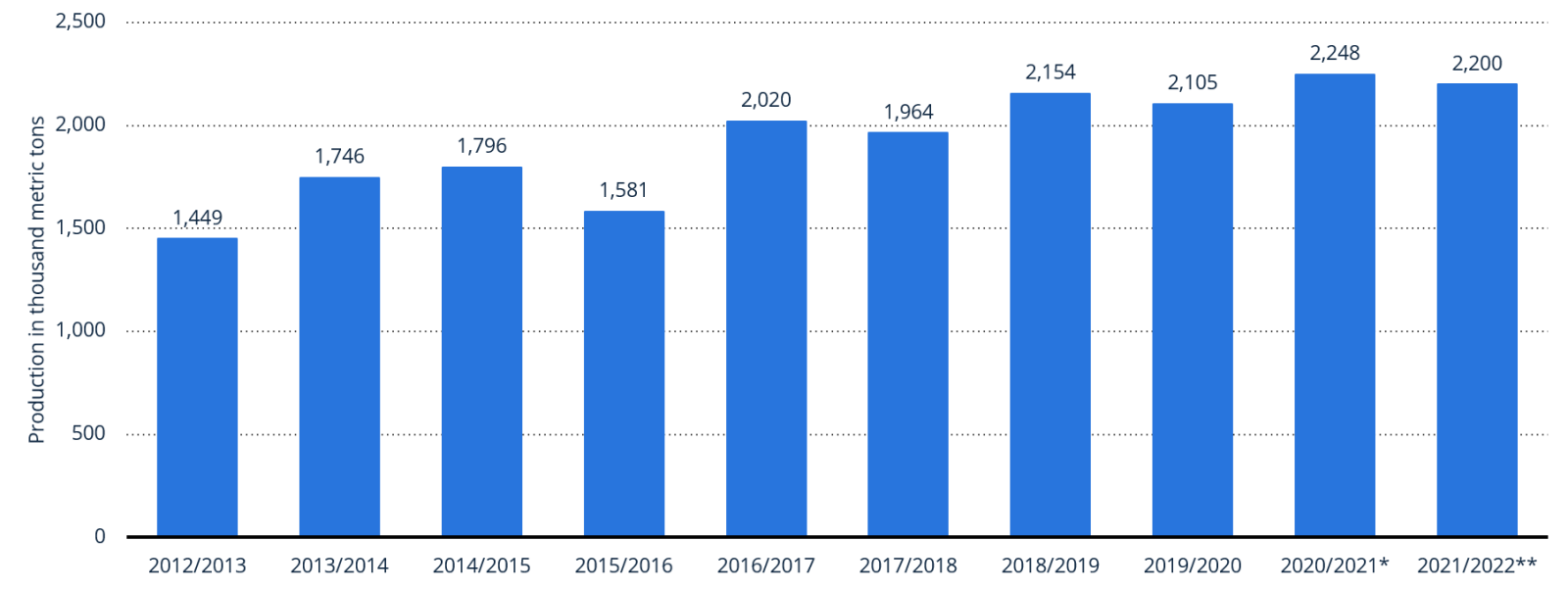

As shown in figure 2 (below), the coca industry has seen tremendous growth through the years, producing at least 1.45 million tons of cocoa beans in 2012/2013. Though it experienced a decline between 2017 & 2018, it recovered from 2018/2019 to reach its highest peak ever in 2021/2022 with production of 2.2million metric tons.

Figure 2: Production of cocoa beans in Ivory Coast from 2012 to 2022 (in 1,000 metric tons)

However, the country’s industry has been affected by swollen shoot virus which has forced many farmers to cut most of the trees, affecting productivity. As of 2018, 23,000 hectares of cocoa were uprooted in just two months.

Ghana

Between 2019-2020, Ghana (the world’s second biggest cocoa producer) is forecast to produce 850,000 tons of cocoa, at the lower end of average levels on account of the swollen shoot disease outbreak. In fact, Ghana cut its crop forecast by 11% because of the disease, which has affected at least 16% of the country’s cocoa crops.

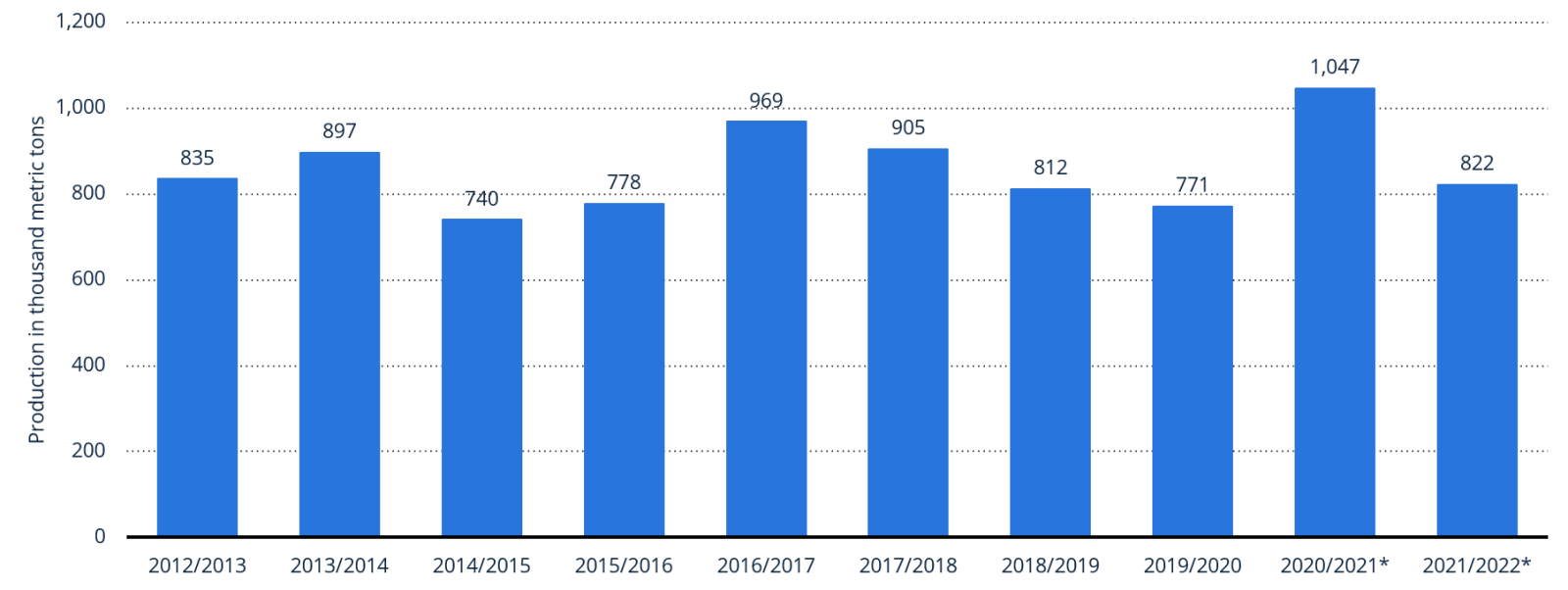

Figure 3: Production of cocoa beans in Ghana from 2012 to 2022 (in 1,000 metric tons)

As shown in figure 3 (above), Ghana experienced a decline in Cocoa production. Between 2021/2021, Ghana is estimated to have produced about 822 thousand tons of cocoa beans, a decrease from approximately 1,047 thousand tons in 2020/2021. This coincided with an out-break of swollen shoot disease, highlighting a very real problem that needs urgent solutions.

This issue presents a major threat for the cocoa industry, and if not checked, productivity is likely to continue declining.

Just like in Cote d I’voire, most cocoa farmers are poor families with not much money to invest in their farms. The use of fake, uncertified fertilizers and pesticides continues to lower farm productivity due to their impact on the soils.

Nevertheless, demand for cocoa continues to grow both domestically and internationally as some locals start to set up factories to capitalize on the local market and international brands continue to demand more cocoa in order to keep up with growing demand for chocolate products globally.

On the other hand, such a problem also presents business opportunities for market entrants offering products and services that have potential to naturally boost the immunity of crops as well as soil productivity.

Are you trying to invest in Ghana’s flourishing cocoa industry? Our specialist market researchers in Uganda can help you conduct an opportunity analysis to help you understand all available opportunities within the cocoa sector in Africa.

Nigeria

Nigeria is the third largest cocoa producing country in Africa, exporting 85% of its annual produce. As of 2018, Nigerian farmers earned about N179 billion from export of raw cocoa beans. However, analysts predicted the 2018-2019 produce to decline 10,000 MT due to extreme weather conditions, pests and diseases plus lower use pesticides which all result in lower yield. Indeed, between 2019 and 2020, Yearly production in tonnage nosedived from about 300,000 metric tonnes in 2013/2014 to 245,000 metric tonnes.

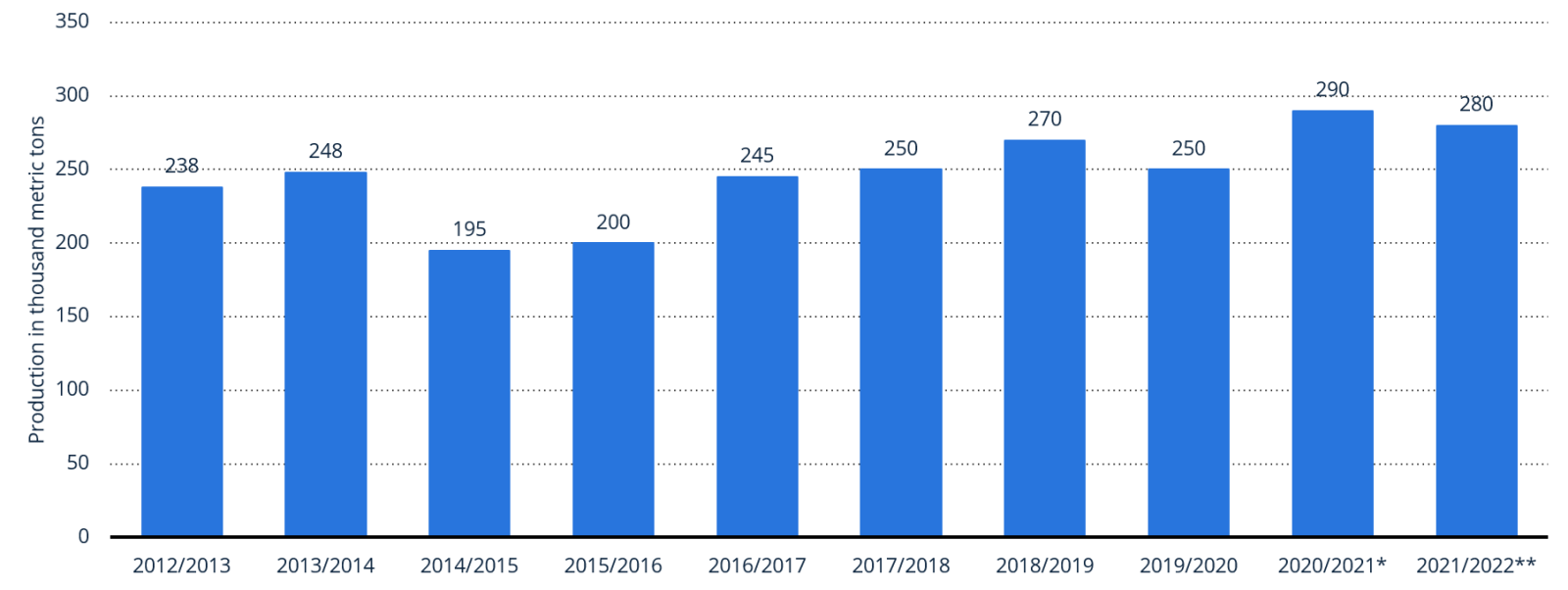

Figure 4: Production of cocoa beans in Nigeria from 2012 to 2022 (in 1,000 metric tons)

Nigeria's mid-crop cocoa output is expected to rise following higher than expected rainfall which has helped boost output for the 2020/21 season to an estimated 320,000 tonnes. Today, some farmers in the Nigerian state of Ondo have doubled cocoa production per hectare, producing one kilogram of cocoa per tree due to the support given to local farmers by the government.

As the government works on increasing productivity, there are many available opportunities for businesses that have potential to boost production through increasing yields.

Our specialist market research analysts in Kampala can help you glean more insights into the available investment opportunities in the African cocoa sector through market research. Get in touch for an opportunity analysis and demand forecasting report on the Nigerian cocoa sector.

Cameroon

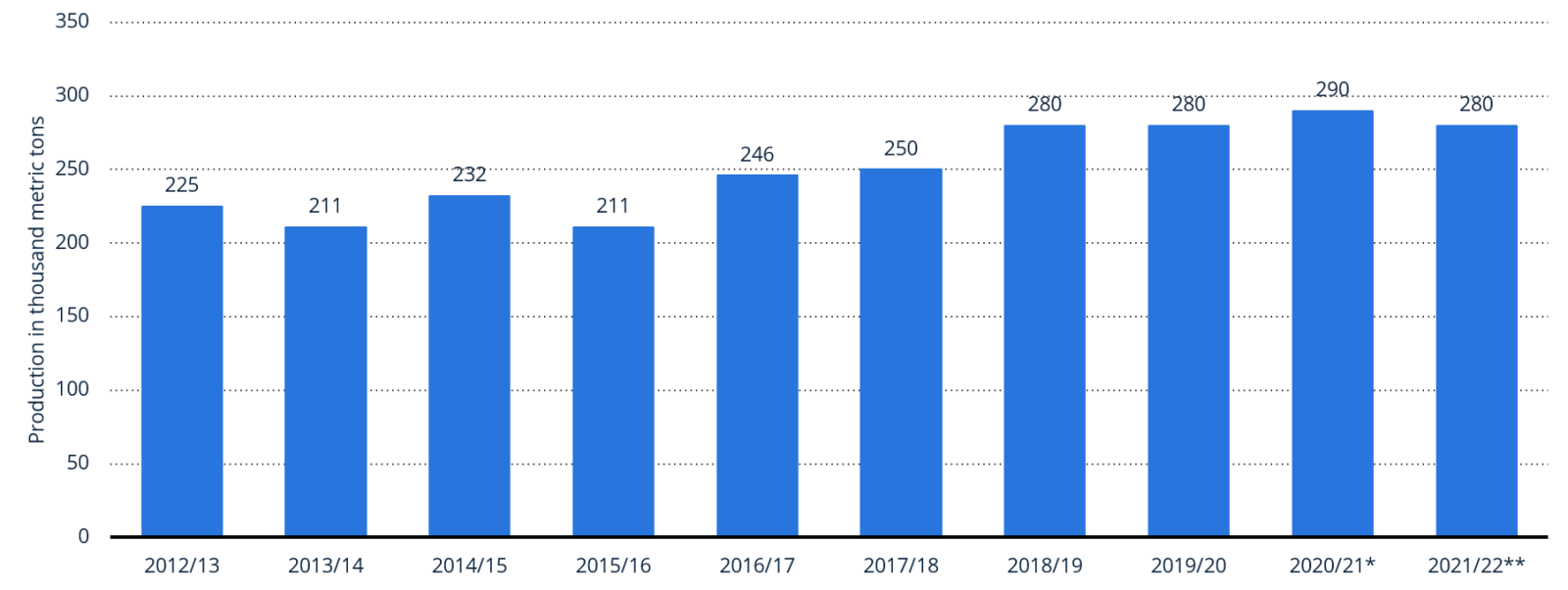

Cameroon is the 4th largest cocoa producing country in the world (behind Ivory Coast, Ghana and Ecuador) and the 3rd largest in Africa with 290,000 metric tons in 2020/2021 season. The nation’s ambition is to lift this to 640,000 MT per year by 2030.

Between 2017 and 2018, the country produced at least 253,510 tons, a volume up by 22,000 tons, compared to the 231,510 tons marketed during the previous campaign. Between 2014 and 2018, the volume of yearly cocoa production in Cameroon rose from 281,000 tons to 336,000.

Cocoa plays an important role in the country’s economy as it is the second largest export product. However, over the last two decades, the quality of the Cameroon cocoa decreased due to a lack of sectoral support. Specialists believe that the country may miss its target of 640,000 tons by 2030. Analysts note that the Southwest has already lost its place as the nation’s leading cocoa producing region. This region’s cocoa sales dropped from 45.45% to 32% during the 2017-2018 campaign, representing a decrease by 43,000 tons.

Irregular rains and prolonged dry seasons resulting from climate change have sucked the moisture from the soil, killed cocoa trees, and cut the yield from his farm. This is one major challenge that is currently forcing most Cameroonian farmers to even change their focus to other products such as rubber. The country faces an uphill battle to meet its long-term target to boost cocoa output to over 300,000 tonnes annually.

Figure 5: Production of cocoa beans in Cameroon from 2012 to 2022 (in 1,000 metric tons)

The number of households owning cocoa trees is between 250,000 and 600,000. Marketed production is estimated at 241,000 t of dry beans for the season 2018-2019, of which 186,000 tonnes were exported without being processed and 55,000 tonnes were sold to local processors.

Conclusion

Despite the fact that market trends show growing global demand for chocolate due to increasing awareness of the potential health benefits of dark chocolate and rising disposable incomes in emerging economies, the African cocoa industry continues to experience a number of challenges. Among the many challenges, the prevalence of pests, diseases and volatile weather continue to limit the potential of the market.

Nevertheless, the market presents opportunities for established companies and market entrants offering products and services that have potential to naturally boost the immunity of crops and enhance yields.

If you are interested in exploring available opportunities in any African country market, our specialist Africa market researchers can help you conduct an opportunity and gap analysis to help you understand the available opportunities based on sound data and robust insights that you can leverage for effective decision making.

Whatever Your African Market Research Needs are, We Can Help. Call Today for a Consultation! Let Our Experts Give You the Information You Need. Talk to Africa’s Expert Market Researchers Today.